Understanding Repo Impact on Credit Reports

A repossession can be a daunting experience. It leaves a mark on your credit report, affecting your financial future. Understanding how a repo impacts your credit is crucial.

Repossession can lower your credit score significantly. This derogatory mark can linger on your credit report for years.

Knowing the duration a repo stays on your credit report is vital. It helps in planning your financial recovery.

This guide will explore the repo process and its effects on credit. We’ll also discuss strategies to rebuild your credit.

By understanding these aspects, you can better manage your financial health. Let’s dive into the details of repossession and credit reports.

What Is a Repossession and How Does It Happen?

Repossession occurs when a lender takes back an asset from a borrower. This usually happens after a series of missed payments. The asset is often something like a car or a house.

Lenders have the right to repossess due to terms in the loan agreement. Once you default, they can reclaim the asset without legal action. However, the details can vary based on state laws.

Here’s a simple breakdown of the repossession process:

- Borrower misses payments.

- Lender sends a default notice.

- Asset is repossessed if payments aren’t resumed.

Understanding the process can help you take proactive steps. Communication with your lender can sometimes prevent repossession. Many lenders offer payment flexibility if you ask early enough.

Repossessions are not just limited to cars. They can also occur with other secured loans. Recognizing the risks involved with different loan types is essential. This knowledge can guide you in better financial management.

Types of Repossession: Voluntary vs. Involuntary

Repossession can occur in two main forms: voluntary and involuntary. Each has unique characteristics and implications.

Voluntary repossession happens when a borrower willingly returns the asset. This might occur when someone realizes they can no longer afford payments. Voluntarily surrendering an asset may seem like a responsible choice when confronting financial troubles.

Involuntary repossession is when the lender takes the asset without the borrower’s consent. It typically involves a sudden collection process, often without prior notice. Both types of repossessions have similar durations on a credit report.

Here’s a comparison of the two:

- Voluntary: The borrower initiates the return.

- Involuntary: The lender reclaims the asset forcefully.

Understanding these differences can help you decide the best action. Sometimes, choosing voluntary surrender can slightly reduce the stress involved.

How a Repo Affects Your Credit Score

When a repossession hits your credit report, expect a noticeable drop in your score. This drop can be over 100 points, and it often depends on your credit health prior to the event. If your credit was high before the repossession, the impact might be more severe.

A repossession is considered a derogatory mark. Lenders view this negatively, as it signals potential financial instability. Such a mark can make future borrowing more challenging and costly.

On your credit report, repossessions appear under negative items. They impact your payment history, which is a major component of your score. Maintaining a positive payment history post-repo can gradually improve your score.

Here are factors that contribute to credit score impact:

- Severity of the repo: Amount owed and recency

- Credit health pre-repo: Higher scores drop more

- Ongoing credit habits: Paying on time post-repo helps recover

To mitigate impact, focus on rebuilding your credit score. Responsible financial behavior over time can lessen a repo’s effect.

Repo on Credit Report Duration: How Long Does It Stay?

A repossession can linger on your credit report for quite some time. It typically remains for seven years. This duration starts from the date of your first missed payment that led to the repossession.

The Fair Credit Reporting Act (FCRA) regulates how long such negative information can stay on your report. After seven years, the repossession should be automatically removed. However, keep an eye on your report to ensure this happens as expected.

Over time, the impact of a repossession on your score lessens. This is particularly true if you maintain good credit habits. Paying bills on time and reducing debt can gradually boost your score.

It is crucial to understand that both voluntary and involuntary repossessions have the same duration on credit reports. The type of repossession does not alter the time it remains as a mark.

Here are key points regarding repossession duration:

- Stays for seven years from first missed payment

- Regulated by Fair Credit Reporting Act (FCRA)

- Both voluntary and involuntary types last the same duration

Despite its presence, you can rebuild your credit over time. With patience and consistency, positive changes in your credit habits will help. Remember to regularly check your credit report to monitor improvements and ensure accuracy.

Lastly, consider disputing any inaccuracies you find related to the repossession. Ensuring the information is correct can help support a healthier financial future.

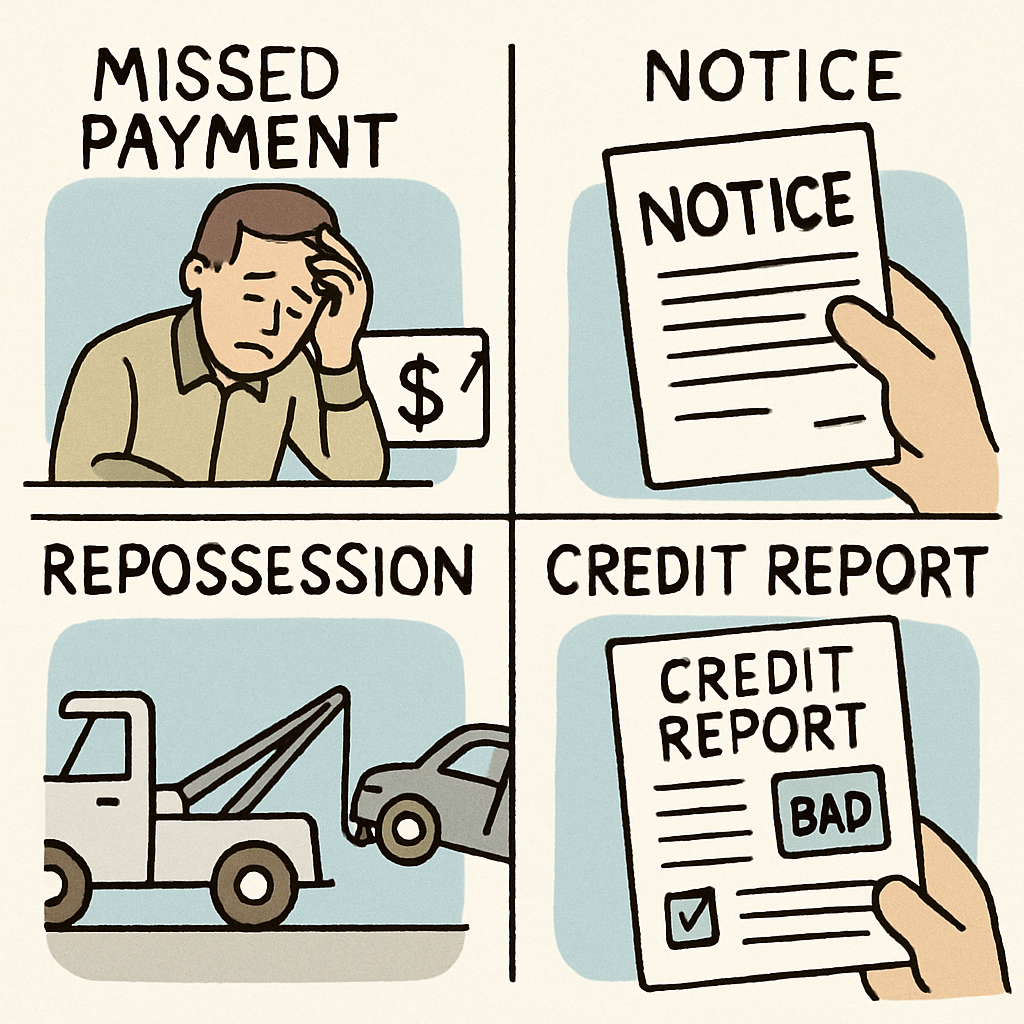

The Process: From Missed Payment to Credit Report

A repossession is not an instant occurrence. It unfolds gradually, triggered by a missed payment. Once you miss a payment, the lender initiates the repossession process. Typically, lenders will notify you and attempt to rectify the situation first.

If payments remain overdue, the lender may repossess the asset. The repossession can be voluntary, where you return the asset willingly, or involuntary, where the lender recovers it without your consent.

Following repossession, the lender usually sells the asset. If the sale doesn’t cover the remaining loan balance, you might face a deficiency balance. This balance adds a negative mark to your credit report.

Finally, the lender reports the repossession to credit bureaus. This entry appears on your credit report, affecting your score. The cycle from missed payment to credit report entry typically spans several months, so it’s critical to act quickly in case of financial distress. Communicating with lenders may provide solutions that prevent repossession and preserve your credit.

Can You Remove a Repo from Your Credit Report?

Removing a repossession from your credit report is challenging, but not impossible. The key is verifying the accuracy of the reported information. Mistakes in reporting can provide grounds for removal.

First, request your credit report from all major credit bureaus. Check for errors in dates, amounts, or other details related to the repossession. If inaccuracies exist, you can dispute these with the credit bureau.

The credit bureau investigates your dispute by contacting the lender. If they find errors, they must correct or remove the repossession from your report. Remember, accuracy is crucial in these disputes.

Apart from inaccuracies, you might consider negotiating with the lender. Some lenders may agree to remove the negative mark in exchange for settling your deficiency balance. However, this depends on the lender’s policies and is not a guaranteed solution.

- Verify the accuracy of the repossession details

- Dispute incorrect details with credit bureaus

- Consider negotiating with the lender

Rebuilding Credit After a Repossession

Rebuilding credit post-repossession requires patience and strategy. The first step is maintaining a budget and ensuring timely bill payments. Consistency in financial habits is key to recovery.

Paying off any outstanding balances from the repossession aids in credit repair. This might also improve lender perceptions. When any debt is settled, focus shifts to current obligations.

Utilizing secured credit cards can be beneficial. They offer a controlled way to manage credit while demonstrating responsible usage to credit agencies. It’s a practical start without a significant credit risk.

Additionally, regularly monitoring your credit report helps identify improvements and remaining challenges. Staying informed allows for targeted action and often prevents future errors.

Credit counseling services provide guidance tailored to individuals’ financial situations. Advisors can help in crafting a realistic plan for debt repayment and improvement of credit health.

- Maintain punctual bill payments

- Settle outstanding balances

- Use secured credit cards wisely

- Monitor your credit report consistently

How to Avoid Repossession in the Future

Avoiding repossession starts with understanding your financial commitments. Keeping a close watch on your income and expenses can prevent you from missing payments. Being proactive when financial challenges arise is crucial.

Communicating with lenders can help when you face temporary financial difficulties. Many lenders offer hardship programs that can provide payment flexibility or temporary relief. Such programs can make the difference in retaining your property.

Building an emergency fund is another essential step. This buffer can cover unforeseen expenses without disrupting regular payment schedules. With a savings cushion, unexpected costs are less likely to lead to financial distress.

- Understand your financial obligations

- Communicate with lenders early

- Establish an emergency fund

Frequently Asked Questions About Repo and Credit Reports

When dealing with repossessions, many people have common questions. Understanding these can clarify the impact on your credit report. Here are answers to some frequently asked questions.

- How long does a repossession stay on a credit report? It remains for seven years.

- Can repossession be removed early? You can dispute inaccurate entries.

- Does repossession affect co-signers? Yes, it impacts their credit too.

Knowing the answers to these common questions can better prepare you for managing your financial future after a repossession. It’s essential to stay informed.

Key Takeaways and Next Steps

Facing a repossession can be challenging, but understanding its impact is crucial. Being informed empowers you to navigate these financial waters more effectively.

Consider these key points to guide your next steps:

- Monitor your credit report for accuracy.

- Dispute any incorrect information promptly.

- Focus on rebuilding your credit with good habits.

By taking proactive measures, you can mitigate the long-term effects of a repossession. Begin your journey towards financial recovery with confidence and informed decision-making.